Remember those math problems back in high school where you had to find the mean, median, and mode? Those exercises were our first real introduction to the idea that a single average number could represent a mountain of data.

But even then, we knew the average didn't tell the whole story. If half the class scored 100% and the other half scored 0 percent, the mean would be 50%. That is a number that doesn't actually represent a single person in the room. In statistics, we call that a deviation. In structural engineering, we call it stress tolerance.

In your finance department, we call it a tolerance threshold in accounts payable.

What Are Tolerance Thresholds in Accounts Payable?

A tolerance threshold in accounts payable is a predefined limit of acceptable variance between an invoice, a purchase order (PO), and a goods receipt. When the difference between these documents falls within the configured threshold, the system treats the invoice as valid and allows it to pass through without manual review.

In practical terms: if a PO says $10,000 and an invoice arrives for $10,085, an AP system with a 1% tolerance threshold ($100) will auto-approve that invoice.

These thresholds are embedded into the validation logic of ERP and AP automation systems. They are applied during two-way or three-way matching before any human review occurs.

When Deviation Becomes Policy in Accounts Payable

Tolerance thresholds in Accounts Payable are a lot like those stress tolerances in engineering. You design for a certain degree of deviation because perfect alignment isn’t practical or efficient. But the moment that tolerance becomes the default rather than the exception, the structure doesn't fail immediately. It just starts to drift.

AP systems operate on a similar premise. Invoices, purchase orders, and goods receipts rarely align perfectly. There are rounding differences, tax treatments that vary by jurisdiction, pricing adjustments, and timing gaps between receipt and billing. Tolerance thresholds exist to absorb this variability and keep the system moving.

The problem isn't their existence. The problem is how much we rely on them without fully understanding what they’re actually doing beneath the surface.

Benefits of Tolerance Thresholds in AP Processing

Before examining the risks, it's worth being precise about what tolerance thresholds do well. When properly configured, they deliver measurable operational value:

- Reduced processing time: Auto-approval of minor variances cuts invoice cycle times. Organizations using AP automation report processing invoices significantly faster than manual workflows.

- Lower exception volumes: Without tolerance thresholds, even rounding differences of a few cents would create exceptions, overwhelming AP teams with noise.

- ERP system compatibility: Most ERPs are built around tolerance-based matching. Thresholds allow these systems to function at enterprise scale.

- Vendor relationship management: Faster invoice processing means faster payments, reducing friction with key suppliers.

What Tolerance Thresholds Actually Do in AP Systems

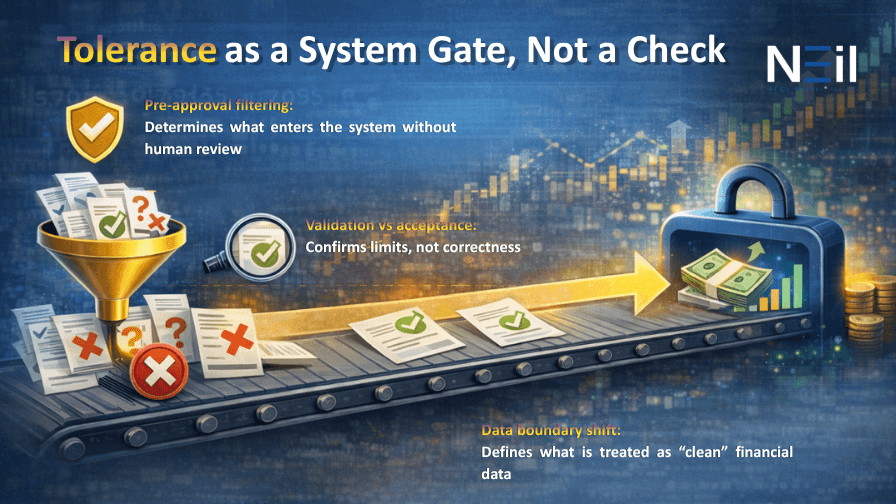

At a technical level, tolerance thresholds are embedded into the validation logic of ERP and AP automation systems. They are applied during two-way or three-way matching to determine whether an invoice can proceed without manual intervention.

It is important to understand that these thresholds aren't validating correctness. They are validating acceptability.

Most systems evaluate tolerance thresholds at multiple levels, often before any human review occurs. Once an invoice passes these checks, it is treated as compliant and flows downstream as a clean transaction. This creates a subtle but critical shift in how data enters the financial system. The boundary of what is considered valid is no longer defined by accuracy, but by predefined limits of deviation.

How tolerance operates inside AP workflows

- Pre-approval gating: Tolerance checks happen before approval workflows, effectively deciding what gets reviewed and what does not.Line vs header evaluation: Variance can be accepted at individual line levels or aggregated at the invoice level, often masking localized discrepancies.

- Static configuration: Most thresholds are fixed percentages applied uniformly across vendors, categories, and geographies.

Once an invoice passes this layer, it is rarely revisited unless flagged by a downstream issue. In effect, tolerance becomes the first and often final filter of data quality.

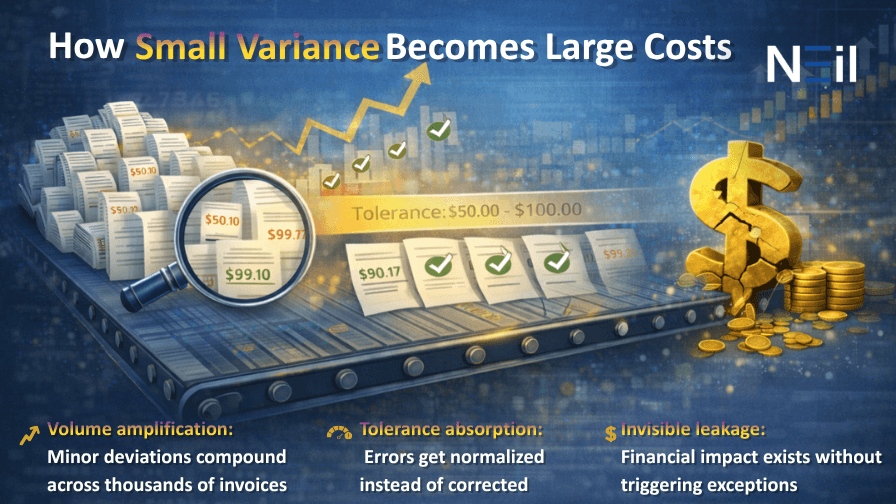

The Economics of Small Variances at Scale

Individually, tolerance thresholds in Accounts Payable appear harmless. A 1 percent deviation on an invoice is rarely material. But AP does not operate at the level of individual transactions. It operates atscale. When small variances are consistently accepted across thousands or millions of invoices, they begin to accumulate into something far more significant, potentially approx 1–3% of annual spend leaking through tolerance absorption in high-volume AP operations.From a financial standpoint, this introduces what can be described as tolerance absorption. Instead of errors being flagged and corrected, they are normalized into the system.

This has several implications:

- Hidden Costs: It creates a layer of cost that isn't explicitly recorded. These aren't errors in the traditional sense, so they don't trigger investigation or correction workflows.

- Working Capital Impact: Even marginal overpayments, when aggregated, affect liquidity and forecasting accuracy.

- Distorted Visibility: The data appears clean, but it isn't entirely precise.

What makes this particularly challenging is that these effects are rarely visible in isolation. They emerge over time, across aggregated data, making them difficult to attribute to any single cause.

Where Tolerance Thresholds in Accounts Payable Becomes a Blind Spot

Tolerance thresholds are designed to reduce friction. But in doing so, they can also reduce visibility. The AP system becomes efficient at processing transactions, but less effective at identifying underlying issues. Over time, this creates blind spots that aren't immediately obvious but have long-term implications.

Patterns where tolerance breaks down

- Systemic drift: Repeated acceptance of small mismatches gradually shifts the baseline of what is considered acceptable, creating structural inaccuracies.

- False positives of validity: Transactions that pass tolerance checks are assumed to be correct, even when they contain underlying discrepancies.

- Masked upstream issues: Problems such as incorrect PO creation, inconsistent vendor data, or tax miscalculations remain unresolved because they fall within tolerance limits.

This is where tolerance transitions from a control mechanism to a masking layer. It doesn't resolve discrepancies. It simply absorbs them.

Risks of Over-Relying on AP Tolerance Thresholds

Understanding the risks is essential for finance teams rethinking their AP validation strategy:

- Audit exposure: Tolerance-passed invoices that contain errors create audit trails that appear clean — until external auditors or tax authorities flag discrepancies.

- Vendor fraud vulnerability: AP systems who understand your tolerance configuration can systematically submit invoices just inside the threshold, accumulating gains over time without triggering a single exception. This contributes to the 3–8% of total AP spend containing recoverable errors that pass tolerance gates undetected

- ERP data integrity degradation: As tolerance-absorbed variances accumulate in the system, financial reporting accuracy declines, particularly in accruals, spend analytics, and cash flow forecasting.

- Compliance risk: For organizations subject to SOX, IFRS, or GAAP reporting standards, systematically accepted variances can create material misstatement risks.

- Duplicate payment exposure: Near-duplicate invoices with slight variations in amount or date can pass independently through separate tolerance checks, creating undetected double payments.

The Structural Limitations of Static Thresholds

Most AP systems rely on static tolerance thresholds. These are predefined percentages or absolute values that apply across all transactions, regardless of context. While this approach simplifies system design, it introduces a fundamental limitation. It assumes that all transactions carry the same level of risk and variability, which is rarely true.

A high-value strategic vendor with consistent invoicing behavior shouldn't be evaluated the same way as a new vendor with irregular patterns. Similarly, different spend categories carry different levels of complexity and risk. Static thresholds ignore these distinctions.

From a systems perspective, this leads to two outcomes. Either the thresholds are set conservatively, resulting in high exception volumes and operational inefficiency, or they are set permissively, increasing the risk of undetected discrepancies. Neither outcome is optimal.

Static Tolerance vs. Context-Aware Validation in AP

The table below compares the two approaches across dimensions that matter most to AP teams and finance leaders:

| Static Tolerance Thresholds | Context-Aware Validation |

|---|---|

| Fixed % or absolute value applied uniformly | Dynamic thresholds adjusted by vendor, category, and risk |

| Binary pass/fail outcome | Probability-based confidence scoring |

| No vendor history considered | Validates against historical transaction patterns |

| Single-dimension check (amount only) | Multi-signal: amount, behavior, tax, timing, category |

| High false-positive rate for complex invoices | Reduced exceptions through smarter pre-filtering |

| Silently accepts all variance within the limit | Flags anomalies within tolerance for contextual review |

| Uniform risk treatment across all vendors | Risk-tiered treatment based on vendor profile |

| Masks upstream data quality issues | Surfaces root-cause discrepancies upstream |

Rethinking Validation: From Thresholds to Context

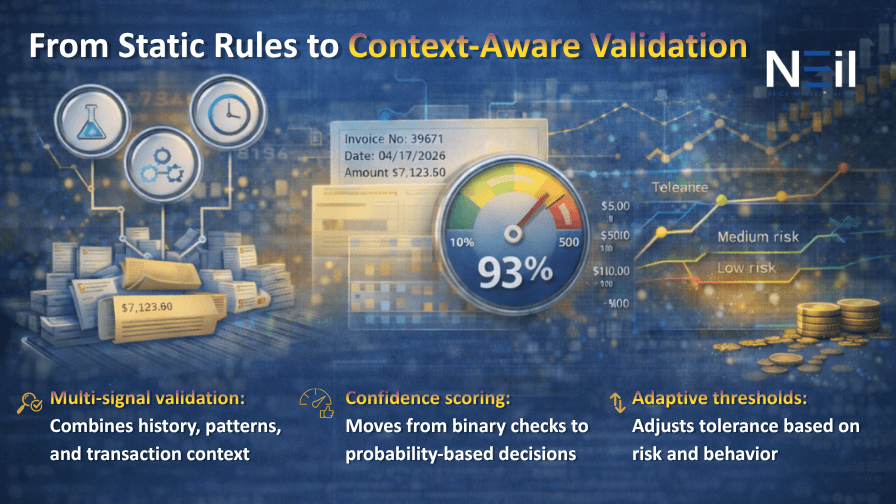

The limitation of tolerance thresholds lies in their binary nature. A transaction either falls within the threshold or it doesn't. There is no concept of likelihood, context, or historical behavior. Modern AP systems need to move beyond this binary model.

Instead of asking whether a transaction is within tolerance, the system should be evaluating how likely it is to be correct based on multiple signals. This introduces a probabilistic approach to validation. Rather than relying on a single rule, the system considers a combination of factors such as vendor history, transaction patterns, tax consistency, and contextual alignment.

What a context-aware validation model looks like:

- Multi-dimensional inputs: Combines invoice data with vendor performance, historical variance, and category-specific behavior.

- Confidence scoring: Assigns a probability of correctness rather than a simple pass or fail outcome.

- Adaptive thresholds: Adjusts tolerance dynamically based on risk signals and past transaction patterns.

Where Neil Fits In

Neil, our AI co-Worker for AP operates as a supervisory layer over AP workflows, focusing on decisioning before transactions are committed to the ERP. Rather than relying solely on static tolerance thresholds, it evaluates invoices using a combination of contextual and historical signals. This includes vendor behavior, transaction patterns, and cross-document consistency.

By introducing multi-signal validation before ERP posting, Neil reduces the reliance on tolerance as the primary filter. It allows the system to differentiate between acceptable variance and potential anomalies more effectively. The result is not the elimination of tolerance, but a shift in how it is used. It becomes one of several inputs into a broader decision-making process, rather than the defining boundary of validity.

To explore Neil, click here

Human-in-the-Loop: A Constrained Form of Oversight

Human intervention is often positioned as the final safeguard in AP workflows. However, in practice, humans only interact with the subset of transactions that fail system checks. This means the majority of transactions, those that pass tolerance thresholds, never receive human review.

From a control perspective, this creates an asymmetry. Humans are responsible for validating exceptions, but they have no visibility into the logic that allowed other transactions to pass. This isn't a failure of human oversight. It is a limitation of how the system defines what requires attention. True control requires visibility into both what is flagged and what is silently accepted.

Designing AP Systems That Go Beyond Tolerance

If tolerance thresholds are necessary but insufficient, the question becomes how to design systems that reduce reliance on them without compromising efficiency. The answer lies in shifting the focus from downstream correction to upstream accuracy and continuous validation.

Principles for moving beyond tolerance-driven systems

- Improve upstream data integrity: Address discrepancies at the source rather than absorbing them during validation.

- Enhance matching intelligence: Move beyond exact and tolerance-based matching toward context-aware reconciliation.

- Implement continuous validation loops: Treat validation as an ongoing process that evolves with transaction data.

This approach changes the role of tolerance. Instead of being the primary mechanism for handling variability, it becomes a secondary safeguard within a more intelligent system.

Closing Thought

Tolerance thresholds in Accounts Payable were introduced to make AP systems practical. They allow organizations to process high volumes of transactions without being constrained by minor discrepancies. But practicality comes with trade-offs.

When tolerance becomes the primary mechanism of validation, it starts to blur the line between efficiency and accuracy. What the system accepts silently becomes part of the financial record, whether it reflects reality or not. The challenge isn't to eliminate tolerance. It is to ensure it doesn't become the default answer to problems that require deeper understanding.

In a system designed to move fast, what gets overlooked is often what matters most.

FAQs

Most companies keep AP tolerance somewhere around 0.5%–3%, or just use a flat amount like $50. It really depends on the type of invoices. Smaller, frequent invoices usually use a fixed amount, while bigger ones use percentages. A single rule for everything usually doesn’t work well.

What is a typical accounts payable tolerance threshold?

Most companies keep AP tolerance somewhere around 0.5%–3%, or just use a flat amount like $50. It really depends on the type of invoices. Smaller, frequent invoices usually use a fixed amount, while bigger ones use percentages. A single rule for everything usually doesn’t work well.

Can tolerance thresholds in accounts payable lead to overpayments?

Yes, and this is where it gets tricky. Small differences that always fall within the limit can quietly add up over time. One invoice isn’t a problem, but thousands can be.

What is the difference between two-way and three-way matching in AP?

Two-way matching is just invoice vs purchase order. Three-way adds the goods receipt, so you know the items were actually delivered. Three-way is safer because it checks one more thing.

How often should AP tolerance thresholds be reviewed?

At a minimum, tolerances should be reviewed once a year. But many companies do it quarterly, especially if there are changes in pricing, vendors, or invoice volume.

Are there industries where AP tolerance thresholds carry higher risk?

Yes, especially in regulated industries like healthcare, financial services, government contracting, or public companies. In these cases, even small discrepancies can lead to compliance issues, audit findings, or problems with financial reporting, not just minor financial leakage.